For the last few years, crypto has been trapped in the same loop.

New token.

New narrative.

New hype.

Same question:

“What pumps next?”

But the biggest money is rarely made by people chasing what is already loud.

It is made by people who catch the infrastructure shift before the crowd realizes the game has changed.

That is exactly why PayFi matters now.

Because while most of the market is still staring at charts, the rails for the next breakout phase of crypto are already being built in plain sight: stablecoins, on-chain settlement, wallet-native payments, cross-border money movement, and real-world merchant utility. This is not a theory anymore. It is not “maybe someday.” The numbers are already screaming it. Visa says stablecoins are becoming increasingly integrated into mainstream payments, and even states that every financial institution should have a stablecoin strategy.

Let that sink in.

When a global payments giant is no longer asking whether stablecoins matter, but instead telling banks they need a strategy, that is not a niche crypto signal. That is a market transition signal. And most people still are not treating it like one. Visa’s recent materials also point to stablecoin circulation above $270 billion, while Reuters reported in January 2026 that Visa’s crypto leadership sees the category growing fast even if merchant acceptance is still early.

This is where the real FOMO should begin.

Because the biggest mistake in every cycle is underestimating the layer that looks “boring” before it becomes essential. DeFi looked niche before it exploded. Stablecoins looked like side tools before they became systemically important. And now PayFi is at that same dangerous stage — the stage where smart builders are moving, while latecomers still think it is too early.

Look at the volume.

(https://a16zcrypto.com/posts/article/state-of-crypto-report-2025)

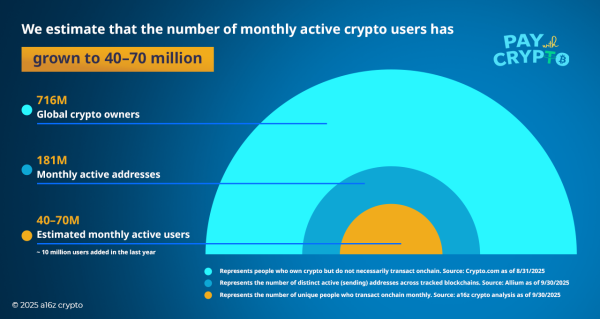

a16z’s State of Crypto 2025 says stablecoins processed $9 trillion in adjusted annual transaction volume, up 87% year over year, with monthly adjusted volume approaching $1.25 trillion in September 2025 alone. That is not small. That is not experimental. That is a financial rail scaling at a speed most people still do not fully understand.

And here is the part the market keeps missing:

When transaction infrastructure starts compounding before the narrative fully matures, the upside does not wait for consensus.

By the time consensus arrives, positioning is already expensive.

That is why PayFi is dangerous — in the best way possible.

Dangerous for people who ignore it.

Dangerous for projects that move too slowly.

Dangerous for anyone still thinking crypto’s future is only about speculation.

Because the next wave is not just about holding digital assets.

It is about using them.

And the addressable market is already massive.

(https://www.triple-a.io/blog/crypto-ownership-report)

Triple-A estimates that 562 million people worldwide owned crypto in 2024, equal to about 6.8% of the global population, up 34% from 2023. Asia alone accounted for 326.8 million crypto holders. That is not a fringe user base anymore. That is a massive, globally distributed, digitally native capital base already primed for the next behavior shift.

Now combine that with where the highest-opportunity users are actually living.

(https://www.binance.com/en/square/post/2024-05-31-2024-5-62-8829064451881)

The UAE has one of the highest crypto ownership rates in the world. Singapore is among the global leaders too. These are not random markets. These are international business hubs, mobility hubs, wealth hubs, travel hubs, and payment innovation hubs. In other words, they are exactly the kind of environments where USDT, stablecoin payments, borderless spending, and wallet-based finance can move from niche behavior to daily habit much faster than people expect.

Then add the lifestyle layer — the one most analysts still underprice.

MBO Partners says the number of American digital nomads reached 18.5 million in 2025, up 153% from 2019. Read that again: 153% growth. That is not a trend. That is a structural shift in how people live, work, earn, and move.

And what do borderless people need?

They do not need another theory.

They need faster rails.

They need to earn globally, hold globally, spend globally, and move capital globally — without getting destroyed by settlement delays, banking fragmentation, unnecessary conversion friction, or outdated payment systems. That is where PayFi stops being a nice idea and starts becoming an inevitable product category.

Because the pain is still there.

The World Bank says the global average cost of sending remittances was still about 6.49% in Q1 2025, far above the UN target of 3%. Think about how insane that is. In 2025, the world still accepts a system where moving money across borders is expensive enough to eat into salaries, freelance income, family support flows, and small business margins. That is not efficiency. That is a giant market inefficiency waiting to be attacked.

And whenever a giant inefficiency meets a scaling new rail, history gets very interesting.

That is exactly what Messari’s PayFi Ecosystem Analysis points toward.

Messari frames PayFi as a multi-layer infrastructure opportunity addressing global payment and financing inefficiencies, and notes that monthly stablecoin transfer volume jumped from $1 trillion to $2.6 trillion in 2024. That kind of acceleration does not happen because a market is “curious.” It happens because demand is already forming underneath the surface.

So ask yourself the real question:

If stablecoin rails are already processing trillions…

If global crypto ownership is already in the hundreds of millions…

If digital nomad and borderless work culture keeps rising…

If cross-border payment friction is still painfully high…

If major financial institutions are telling the world to prepare stablecoin strategies…

What exactly are people waiting for?

Permission?

Consensus?

Another buzzword?

That is how people get left behind.

The market loves to pretend it wants innovation early. In reality, most people only believe once the move is obvious. But obvious is late. Obvious is crowded. Obvious is where retail comes after the groundwork has already been laid by builders, operators, and ecosystems that moved when the signals were still asymmetric.

That is why PayFi feels like one of the most explosive setups in Web3 right now.

Not because everyone already gets it.

But because they do not.

And that gap between reality and recognition is where the biggest upside usually lives.

To be clear, this does not mean the whole stablecoin economy is already pure checkout payments today. Reuters reported that JPMorgan pushed back on the most aggressive long-term forecasts and argued only a relatively small share of current stablecoin demand is directly tied to payments, with much of the rest still concentrated in trading, DeFi, and collateral flows.

But that is exactly why this moment matters.

If the category is already processing enormous volume, already gaining institutional attention, already aligning with borderless user behavior, and still has early penetration in actual payment usage, then the upside is not gone — it may be just beginning.

That is the asymmetry.

The rails are maturing.

The users are forming.

The pain is real.

The market still underprices the shift.

And that is where PayWithCrypto can hit differently.

Because the winners of the next cycle may not be the ones with the loudest slogans. They may be the ones who make USDT spending, QR payments, wallet utility, merchant adoption, and cross-border settlement feel so seamless that users stop calling it “crypto” and start calling it normal.

That is when sectors stop being narratives and start becoming defaults.

That is when habits form.

That is when retention compounds.

That is when distribution matters more than noise.

That is when the real moat begins.

So yes — people can keep chasing the next shiny token.

They can keep waiting until PayFi is “confirmed.”

They can keep pretending stablecoins are just parking tools.

But history is usually brutal to people who confuse early with risky and obvious with safe.

The market has already spent years proving that people are willing to buy digital assets.

The next and much bigger race is about who will help the world use them.

And when that shift fully hits,

the projects that moved first will not be asking for attention.

The next chapter of Web3 will not be won by noise alone.

It will be won by utility.

By repetition.

By daily usage.

By becoming part of how people actually live, spend, move, and transact.

That is why the rise of PayFi matters so much.

Because when stablecoins stop being something people only hold, and start becoming something people use every single day, the entire market changes.

At that point, the winners will not simply be platforms.

They will be infrastructure.

They will be habit.

They will be the rails beneath a new global economy.

And when that moment arrives, PayWithCrypto should not just be participating in the movement.

It should be leading it.

Because the future does not wait for permission —

it belongs to the builders bold enough to create it first.